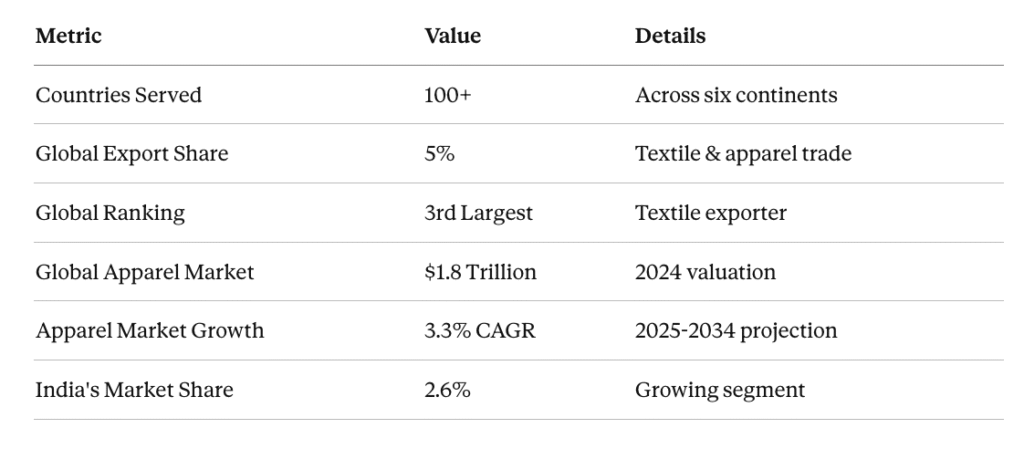

India’s textile industry stands as the world’s second-largest exporter of textiles and apparel, with deep roots in heritage craftsmanship combined with modern manufacturing capabilities. The industry has undergone significant transformation, emerging as a global powerhouse while maintaining its unique identity.

1. NATIONAL TEXTILE INDUSTRY OVERVIEW

1.1 Industry Significance & Scale

The Indian textile industry is the second-largest employment generating sector in India after agriculture. The industry contributes:

- 2.3% to India’s GDP

- 13% to industrial production

- 12% to total exports

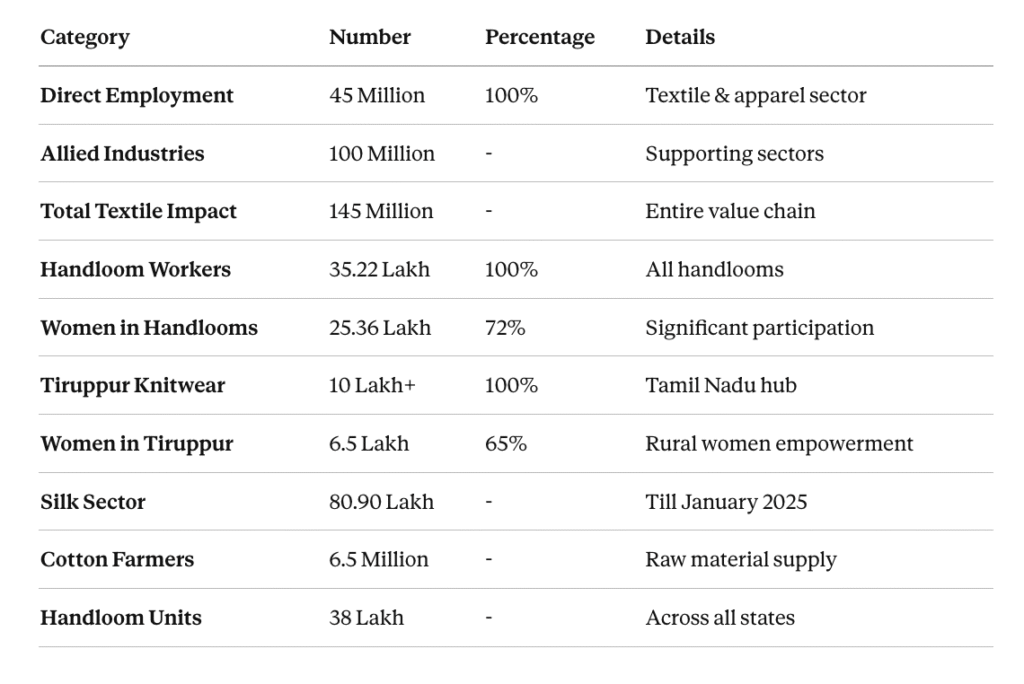

- 35-45 million people directly employed

- 100 million in allied and supportive industries

1.2 Global Position

India maintains a unique global textile position:

- Largest cotton and jute producer globally

- Second-largest silk producer in the world

- Third-largest textile exporter globally

- Fifth-largest technical textiles market globally

- Preferred sourcing destination for major global retailers

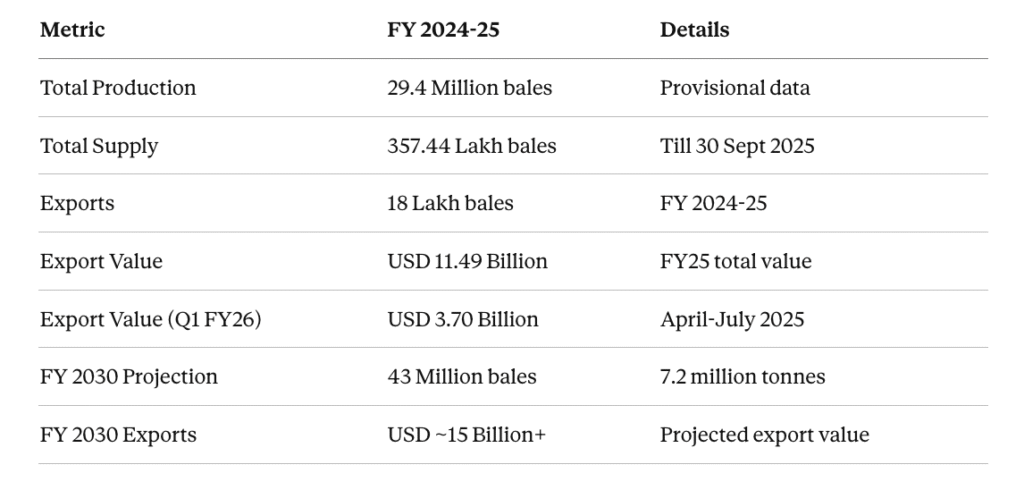

1.3 Annual Production Capacity Figures

2. MARKET SIZE & GROWTH PROJECTIONS

2.1 Domestic Market Growth

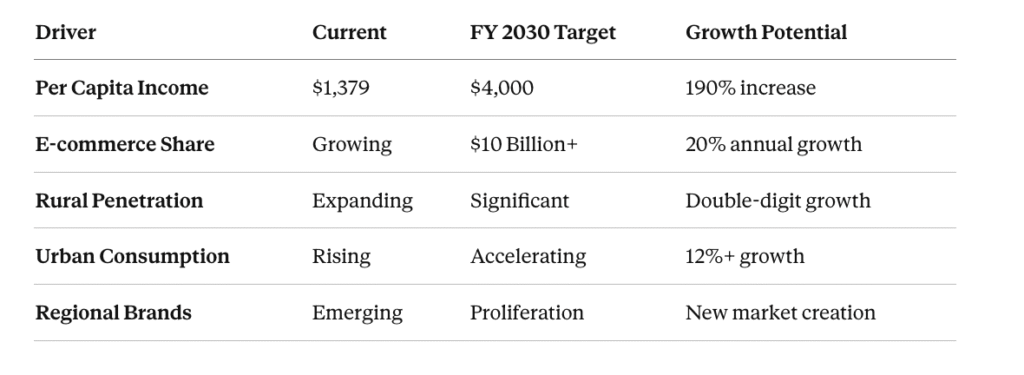

The Indian domestic textile market has emerged as a significant growth driver:

Per Capita Income Growth: USD 1,379 (FY25) → USD 4,000 (FY30), driving consumption increase.

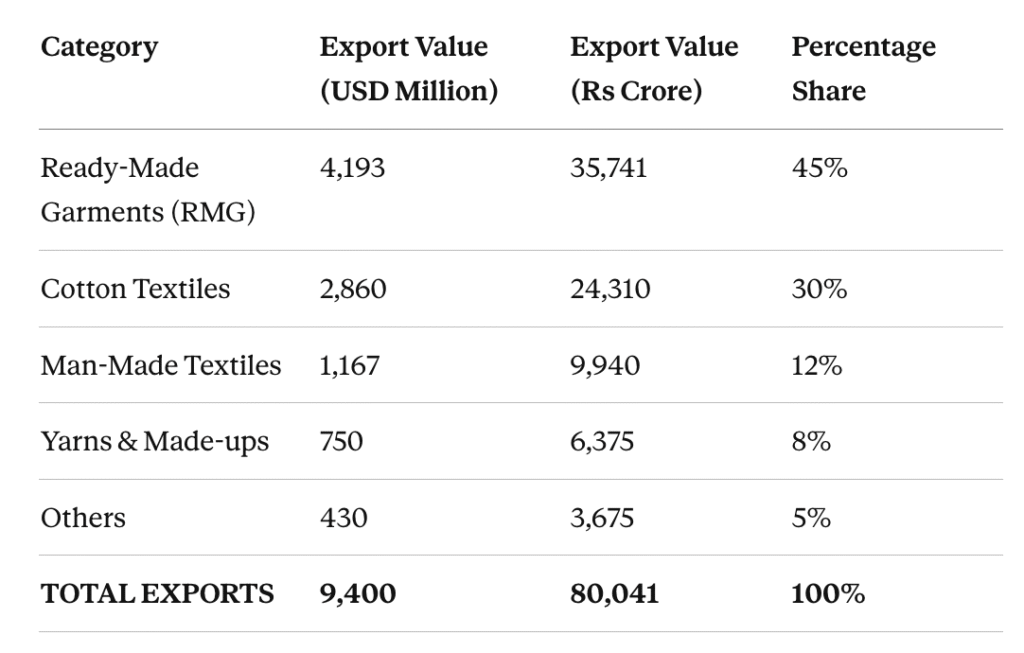

2.2 Export Performance (FY 2024-25)

Total textile and apparel exports in Q1 FY26 (April-June 2025): USD 9.40 billion

Historical Export Trends:

- FY 2023-24: USD 17.3 billion (Apparel: 42%, Raw materials: 34%, Non-apparel: 30%)

- FY 2024-25 (April-July): USD 16 billion in RMG alone (10% growth)

- Apparel exports showing consistent 8-12% year-on-year growth

3. STATE-WISE TEXTILE INDUSTRY ANALYSIS

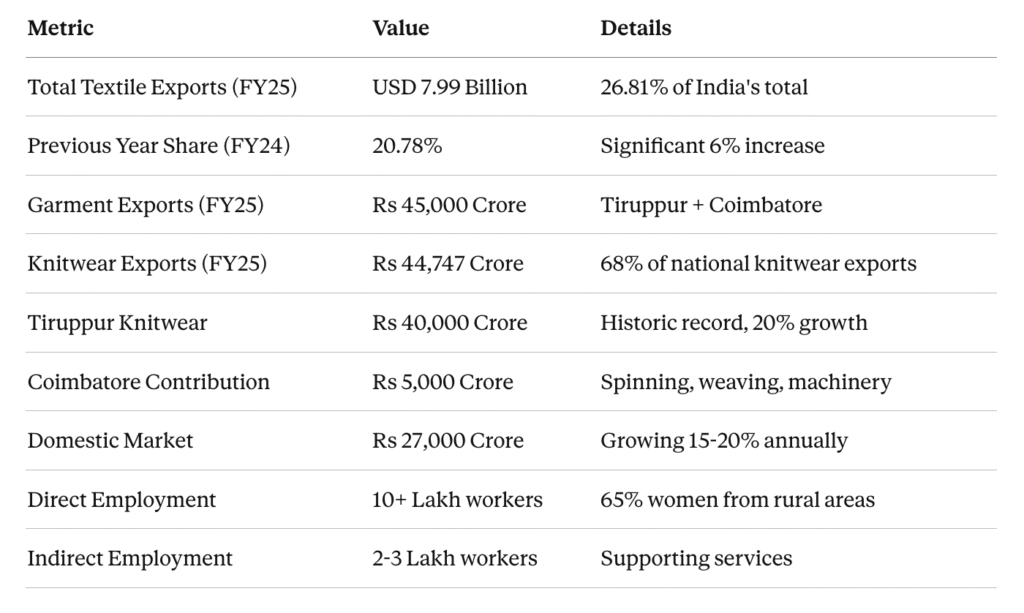

3.1 TAMIL NADU – The Knitwear Capital

Status: India’s leading textile exporting state Global Recognition: Tiruppur – “Knitwear Capital of India”

Performance Metrics

Regional Specializations

Tiruppur:

- 90% of India’s cotton knitwear exports

- 55% of all knitwear exports by volume (national)

- 6 lakh direct workers, 2 lakh indirect

- 65% female workforce, mostly rural origin

- Major clients: Primark, Tesco, H&M, Gap, Walmart, Decathlon

- Global reach: 50+ countries including USA, EU, Australia

- Market recovery: 20% growth in FY25 after -14% contraction in FY24

- Technology: Quick turnaround times (7-10 days), flexible supply chains

Coimbatore:

- Spinning mills and weaving centers

- Textile machinery manufacturing

- Known as “Manchester of South India”

- Dyeing and finishing operations

- Technical textiles production

Erode:

- Power loom operations

- Dyeing and printing facilities

- Fabric finishing

Karur:

- Home textiles production (towels, bed linen, kitchen textiles)

- Exports to major global retail chains (Target, Walmart, IKEA)

- Bed linen and bath textile specialization

Total Employment: 45+ lakh people directly and indirectly

3.2 GUJARAT – The Manufacturing Powerhouse

Status: Manufacturing and technical textiles leader Global Recognition: “Silk City” (Surat)

Regional Specializations

Surat:

- 41,000+ power loom units

- 381 dyeing and printing mills

- 40% of India’s art silk production

- Synthetic fabric manufacturing

- Polyester and man-made fiber textiles

- Rs 600 crore annual synthetic fabric exports (primarily to Dubai)

Ahmedabad:

- Cotton textiles manufacturing

- Saree production

- Shirting fabrics

- Apparel manufacturing

- Textile design and innovation centers

Vadodara:

- Premium denim production

- Eco-friendly dyeing technologies

- Man-made fiber textiles

Umbergaon:

- Modern powerlooms

- Synthetic suiting and shirting

- Export-oriented production

Dahej & Sanand:

- Integrated textile parks

- Industrial clusters

- Facilities for entire value chain

Growth Drivers

- 2.3-fold increase in textile exports since 2012 textile policy launch

- 19% of state’s labor force employed in textiles

- 30% woven fabric from organized sector

- 25% fabric from unorganized sector

- Infrastructure: Ports in Kandla, specialized logistics

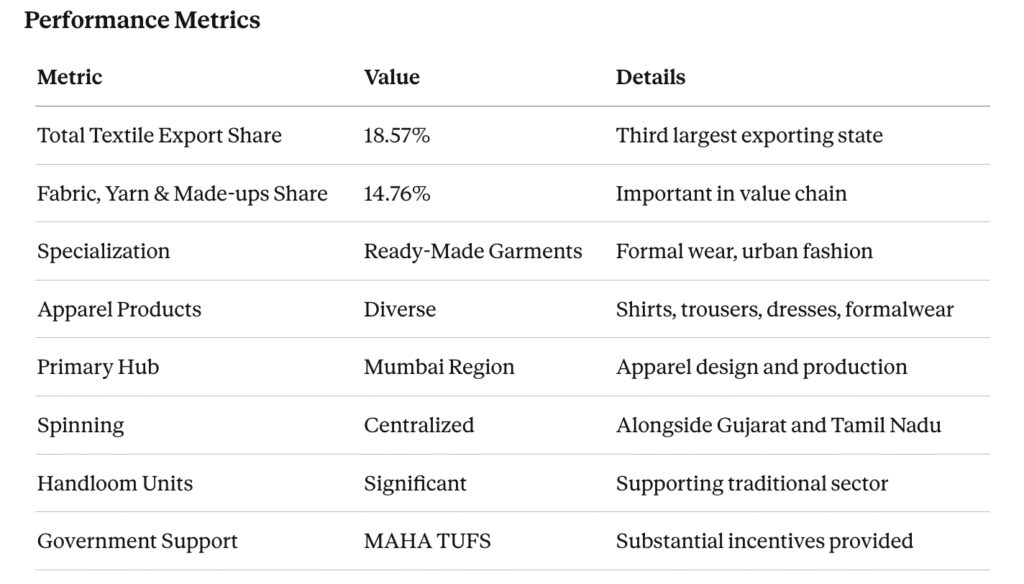

3.3 MAHARASHTRA – The RMG & Spinning Center

Status: Ready-made garment manufacturing hub Primary Focus: Apparel design, production, and finishing

Key Features

- Major center for formal wear and business apparel

- Quality control and international compliance expertise

- Access to global fashion trends

- Strong networking with international brands

- Design and development capabilities

- Vertical integration from fabric to finished apparel

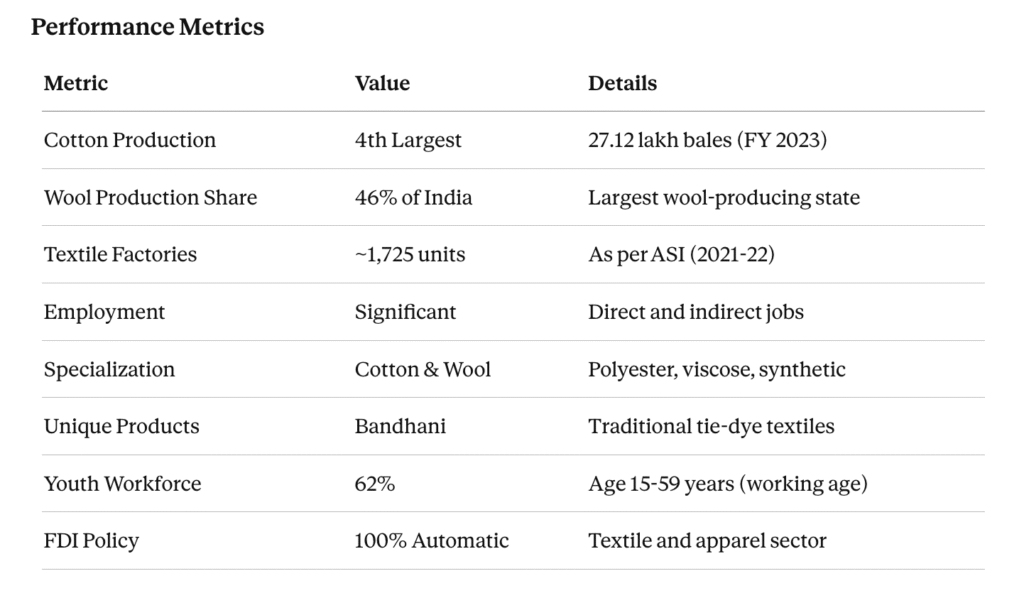

3.4 RAJASTHAN – The Cotton & Wool Capital

Status: Raw material production and specialty textiles Historical Significance: Home to world-famous Bandhani technique.

Regional Focus

- Polyester viscose suiting

- Polyester viscose yarn

- Synthetic suiting material

- Wool and wool-blend products

- Traditional handicraft textiles

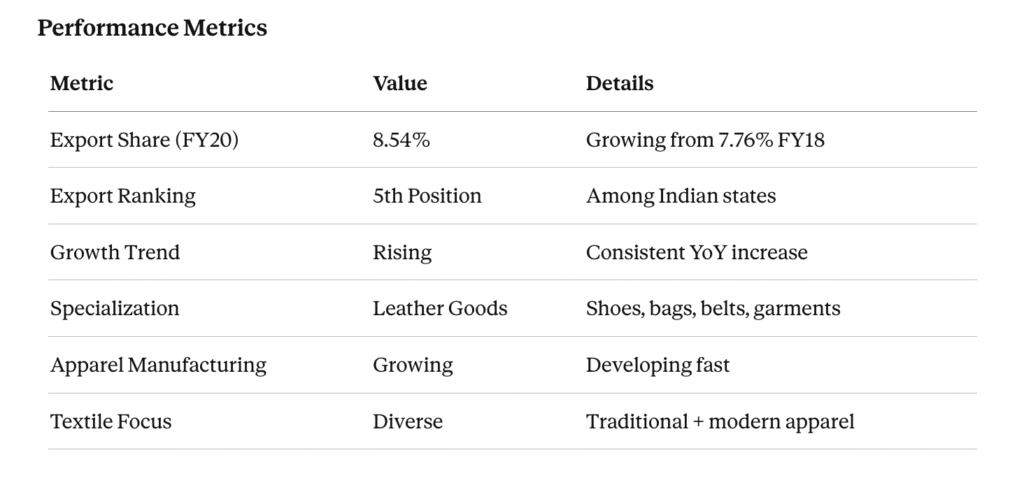

3.5 UTTAR PRADESH – Leather & Apparel Hub

Status: Growing apparel manufacturer Key Hub: Kanpur – “Leather Capital of India”

Kanpur Specialization

- Leather goods manufacturing

- Shoes and footwear

- Leather bags and accessories

- Leather garments

- Embroidered and decorated items

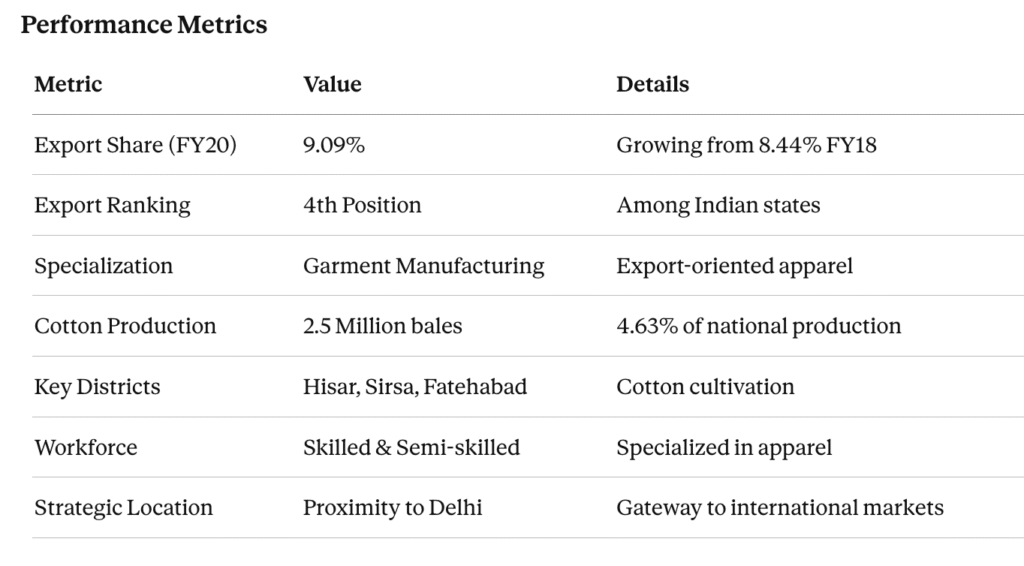

3.6 HARYANA – Garment Manufacturing Hub

Status: Significant export-oriented apparel producer Primary Centers: Gurgaon, Faridabad, Hisar.

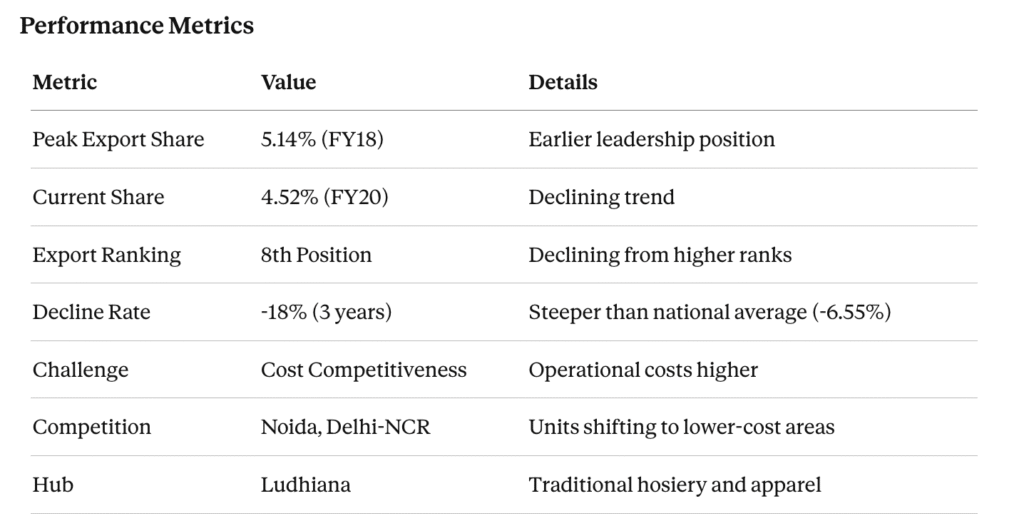

3.7 PUNJAB – Traditional Garment Center

Status: Declining from earlier prominence Challenge: Facing competitive pressure and cost challenges

Challenges Facing

- Rising operational costs

- Wage pressures

- Electricity costs

- Shifting of units to adjacent states

- Competition from Noida and Delhi-NCR

- However: Manufacturing continues, with exports through multiple channels

3.8 Emerging & Other Important States

Telangana

- Emerging as strong textile hub

- Kakatiya Mega Textile Park in Warangal (one of India’s largest)

- Cotton production: 5.31 million bales (3rd largest nationally)

- Leading cotton producer in Southern zone

- Government support: Telangana Textile and Apparel Policy

- Major investments from Welspun Group, Ginni Filaments, others

Andhra Pradesh

- Growing textile manufacturing center

- Brandix India Apparel City (BIAC) in Visakhapatnam

- Multiple textile parks and infrastructure

- Significant cotton production

- Strong in apparel manufacturing

- Ranked among top states for ease of doing business

Karnataka

- Silk dominance: 65% of India’s mulberry silk production

- Largest silk-producing state nationally

- Black cotton soil ideal for cotton cultivation

- Textile machinery industry

- Man-made fiber production

- Research and development centers

Jharkhand

- Tasar silk leading producer

- Growing textile manufacturing sector

- Traditional silk production heritage

- Rapid industry growth

- Ranked high in ease of doing business

West Bengal

- Handlooms sector with strong heritage

- Traditional weaving traditions maintained

- Handicraft production

- Growing apparel manufacturing

- 50+ lakh handloom units concentrated

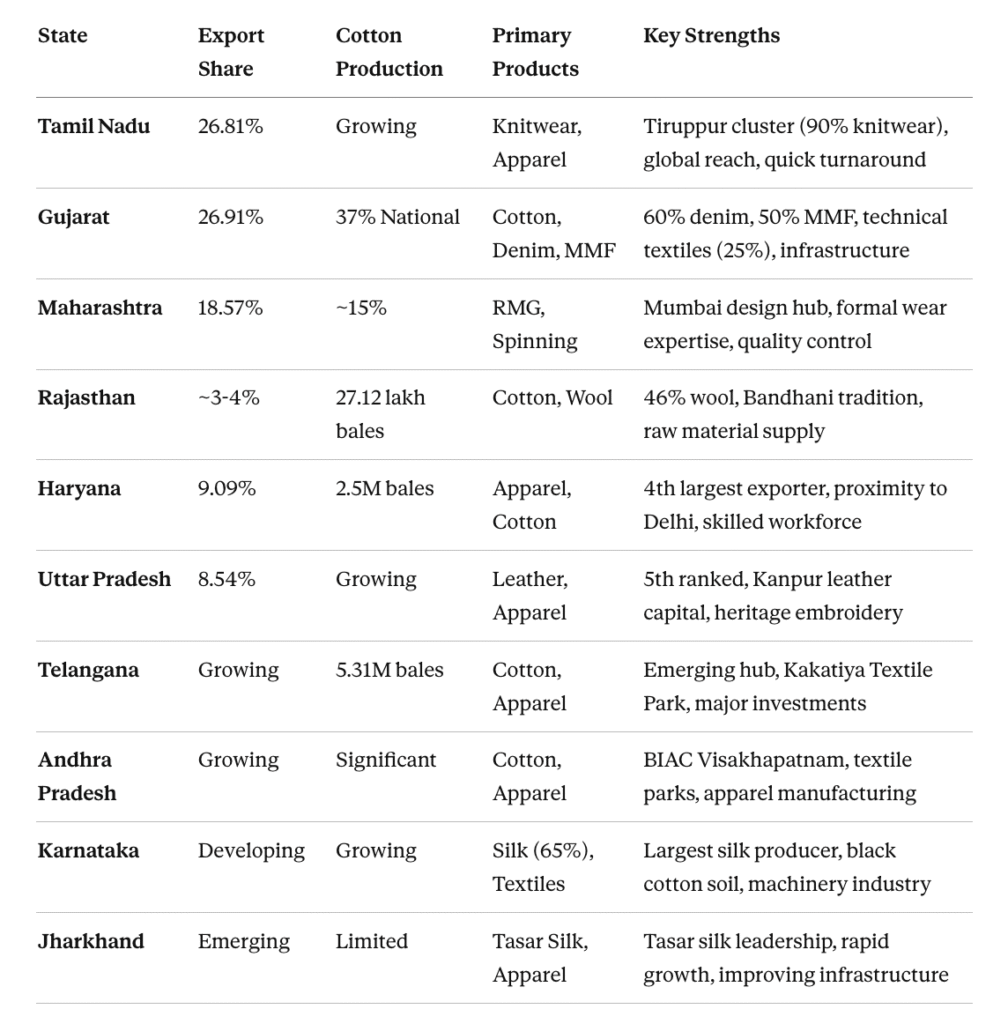

4. COMPARATIVE STATE-WISE PERFORMANCE TABLE

5. COTTON PRODUCTION & DISTRIBUTION

5.1 Top Cotton-Producing States (2023-24)

5.2 Production Zones

Central Zone (Largest – 43% of National):

- Gujarat: 9.49 million bales (Central Zone leader)

- Maharashtra: High contribution

- Madhya Pradesh: Central plains

- Climate: Semi-arid, monsoon dependent

- Infrastructure: Developed textile hubs

Southern Zone (Second Largest – 28.5% of National):

- Telangana: 5.31 million bales (3rd nationally)

- Andhra Pradesh: 7.25 lakh bales

- Karnataka: Moderate production

- Tamil Nadu: Growing production

- Climate: Tropical, monsoon influenced

- Infrastructure: Emerging textile clusters

Northern Zone:

- Rajasthan: 27.12 lakh bales (4th nationally)

- Haryana: 15.09 lakh bales (7th nationally)

- Punjab: Limited production

- Climate: Arid to semi-arid, irrigation-dependent

5.3 Cotton Supply & Export

6. EMPLOYMENT & SKILLS DEVELOPMENT

6.1 Employment Statistics

6.2 Skill Development Initiatives (2024-25)

Training Programs

- Total trained: 1+ million workers annually

- Coverage areas:

- Garment manufacturing

- Digital marketing

- Sustainability practices

- Quality control

- Design and innovation

Handloom Sector Development

Women Empowerment

- Handloom sector: 72% female workforce

- Tiruppur knitwear: 65% women from rural areas

- Income generation: Primary/supplementary household income

- Social impact: Structural employment in regions with limited formal job opportunities

- Skill development: Training and capacity building programs

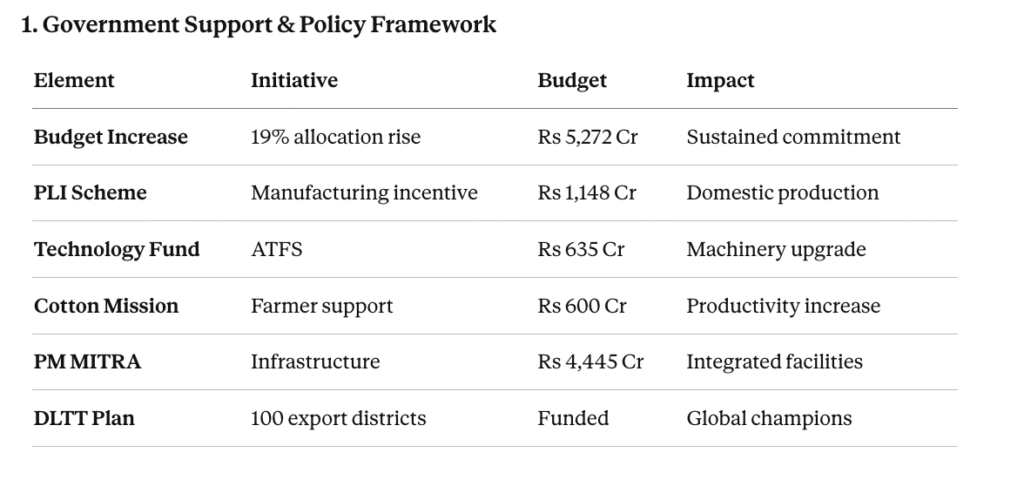

7. GOVERNMENT INITIATIVES & BUDGET ALLOCATION

7.1 Union Budget 2025-26

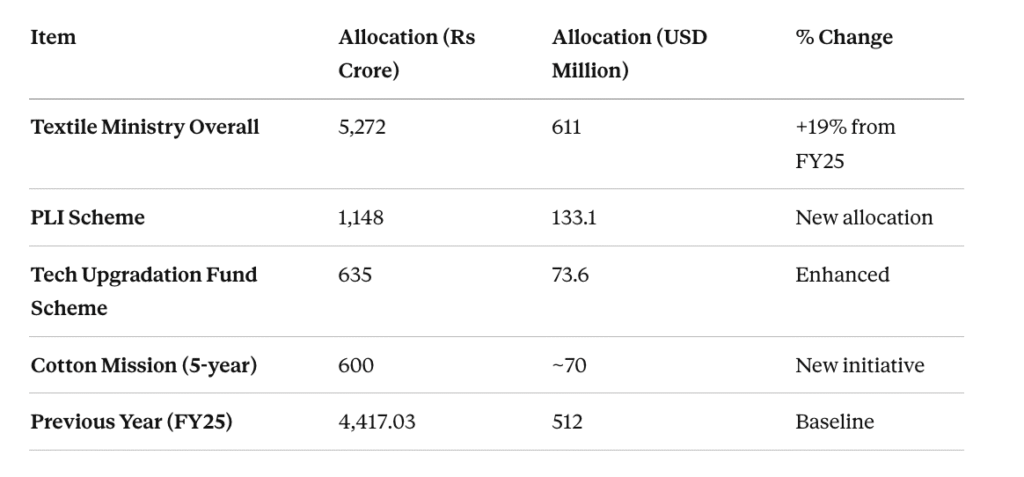

Ministry of Textiles Allocation

7.2 Key Government Schemes (2025-26)

1. Production Linked Incentive (PLI) Scheme

- Allocation: Rs 1,148 crore (USD 133.1 million)

- Objective: Boost domestic manufacturing and exports

- Target: High-value textile products and apparel

- Eligibility: Manufacturing units meeting production targets

- Timeline: Multi-year scheme

2. Amended Technology Upgradation Fund Scheme (ATFS)

- Allocation: Rs 635 crore (USD 73.6 million)

- Objective: Modernize textile machinery and technology

- Focus Areas:

- Benefit: Improved productivity and competitiveness

3. Cotton Mission (5-Year Initiative)

- Allocation: Rs 600 crore (~USD 70 million)

- Objective: Revitalize India’s cotton sector

- Focus:

- Increase cotton productivity

- Support cotton farmers

- Develop improved varieties

- Extension services

4. District-Led Textiles Transformation (DLTT) Plan

- Scope: District-focused strategy

- Target Districts: 100 high-potential + 100 aspirational

- Objective: Develop global export champions

- Focus Areas:

- Skills development

- Infrastructure improvement

- Market linkages

- Special emphasis on Eastern and Northeastern India

5. PM MITRA Park Scheme

- Total Allocation: Rs 4,445 crore

- Objective: Create integrated textile value chains

- Scope: Spinning to finished product manufacturing at single location

- Geographic Coverage: Multiple locations across India

- Features:

- Common facility centers

- Dedicated infrastructure

- Plug-and-play units

6. Handloom & Handicrafts Programs

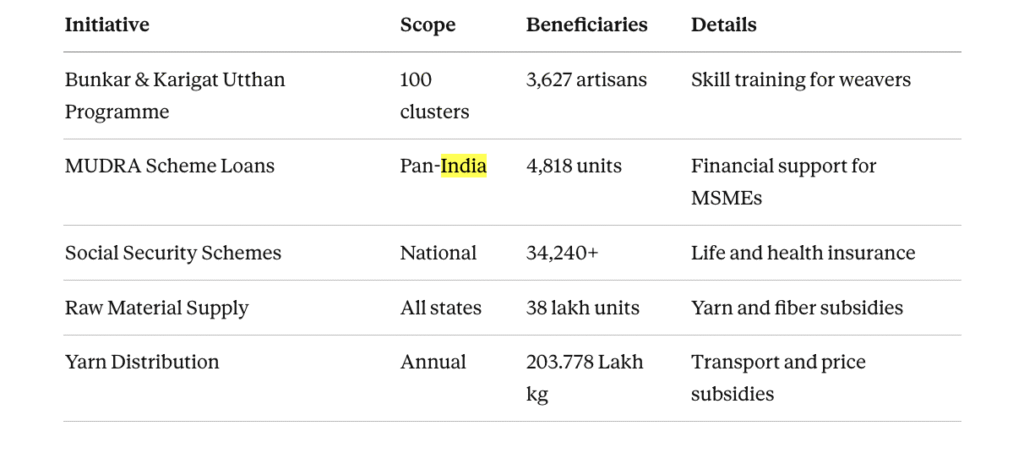

- Bunkar & Karigat Utthan Programme: Skill development of 3,627 artisans across 100 clusters

- 10th National Handloom Day: Celebration and promotion

- Craft Tourism Villages: Development in Uttar Pradesh, Himachal Pradesh, J&K

- Common Facility Centers: For artisans and producers

- E-commerce Platform (indiahandmade.com):

- 9,453 products uploaded

- 1,722 sellers registered

- Direct market access

7. Silk Sector Initiatives

- Eri Silk Project in Gujarat

- Central Silk Board Platinum Jubilee celebrations

- Sericulture advancement programs

- Production enhancement: Till January 2025: 34,042 MT raw silk production

8. Jute Sector Support

- New pricing methodology for jute sacking bags

- Worker and farmer benefit focus

- Modernization initiatives

- Environmental sustainability promotion

9. Make in India Initiative

- Launch date: 2014

- Impact: 2.3-fold increase in textile exports since 2012 textile policy

- Continues to: Position India as global textile manufacturing hub

- Methods: Policy support, infrastructure development, incentives

10. Export Promotion Mission

- Market Access Support Intervention

- Objective: Strengthen global market access

- Methods: Trade facilitation, buyer-seller meets, market research

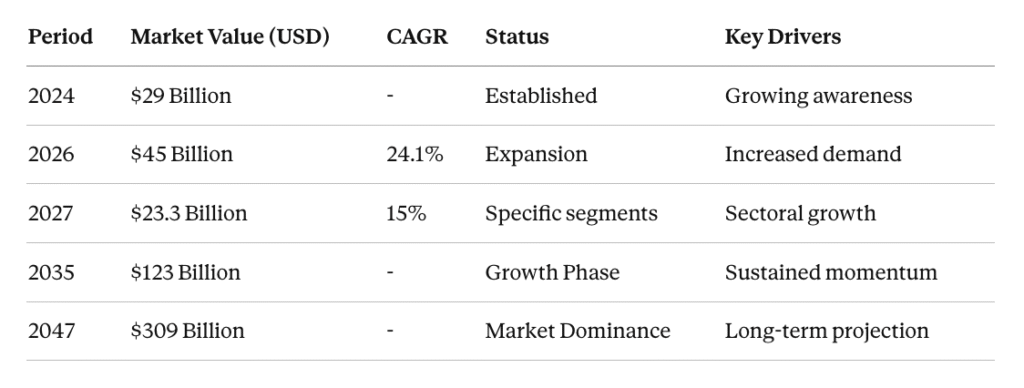

8. TECHNICAL TEXTILES – THE HIGH-GROWTH SEGMENT

8.1 Market Size & Growth Projections

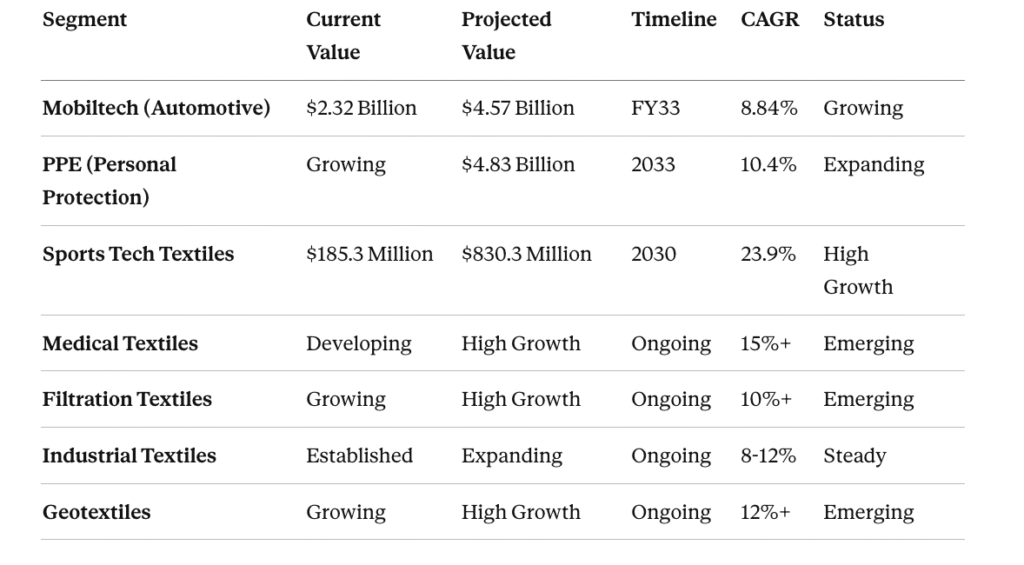

8.2 Key Technical Textile Segments

8.3 India’s Position in Technical Textiles

8.4 Application Areas

- Mobiltech (Automotive): Car interiors Safety components Sound insulation Moisture management Growth: 8.84% CAGR to FY33

- Medical & Healthcare: Surgical textiles Wound care Hospital fabrics Implant materials Growth: Double-digit rates

- PPE (Personal Protection Equipment): Protective clothing Filtration masks Industrial safety wear Growth: 10.4% CAGR to 2033 Status: Second-largest PPE manufacturer globally

- Sports & Performance Textiles: Athletic wear Performance fabrics Moisture-wicking Growth: 23.9% CAGR to 2030

- Industrial & Filtration: Filter fabrics Separation textiles Industrial coverings Environmental applications

- Geotextiles & Construction: Soil stabilization Drainage systems Construction reinforcement Environmental protection

9. GLOBAL EXPORT MARKETS & OPPORTUNITIES

9.1 Key Export Destinations

Primary Markets (High Volume)

Regional Markets (Growing)

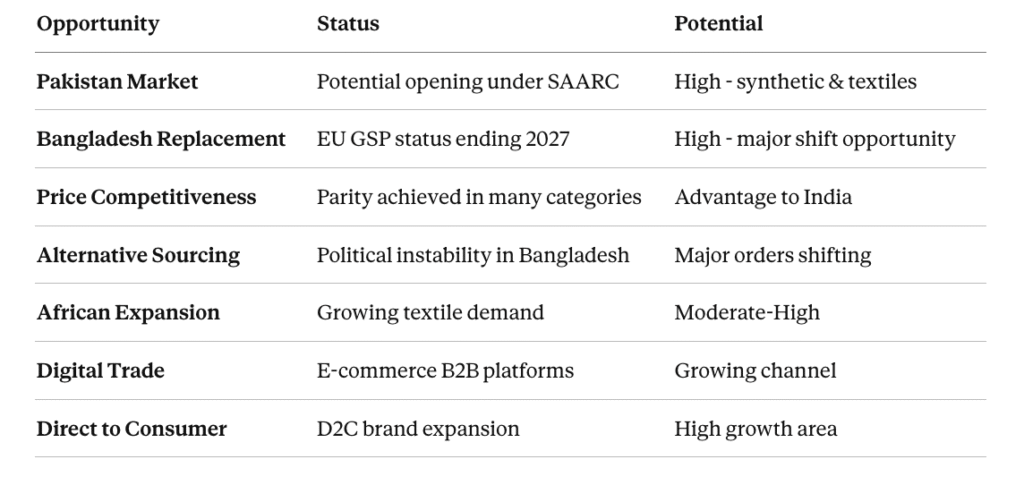

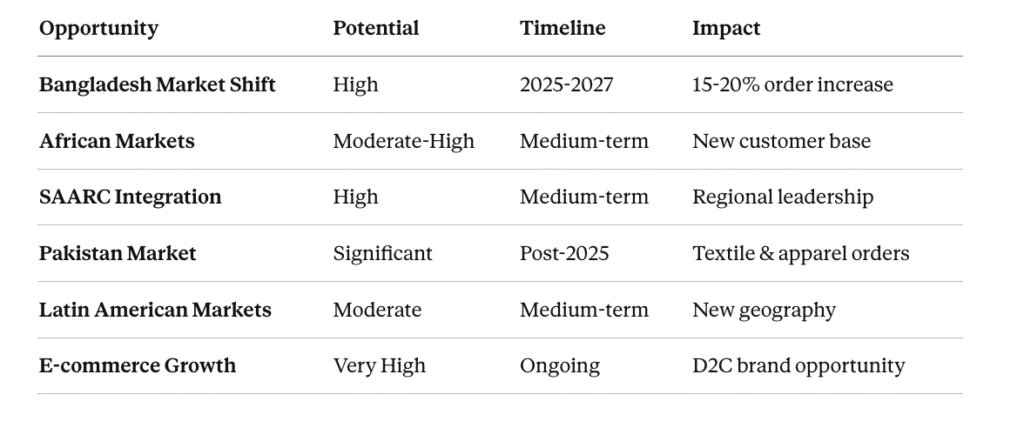

Emerging Opportunities (2025-2030)

9.2 Global Trade Position

9.3 Recent Market Dynamics & Opportunities

Bangladesh Crisis Impact (2024)

- Political Instability: Government changes and social unrest

- Effect on India: Major order shift from Bangladesh to India

- Tiruppur Response: 20% export growth in FY25

- Buyer Actions: Global retailers seeking alternative suppliers

- India’s Advantage: Established manufacturing base, quality reputation

EU GSP Status Change (Post-2027)

- Bangladesh Impact: Losing Generalized Scheme of Preferences with EU

- Timing: Preference withdrawal in 2027

- India Advantage: Position itself as alternative sourcing hub

- Price Dynamics: Achieving parity with Bangladesh in several categories

- Buyer Strategy: Strengthening sourcing base in India

- Market Share: Potential to capture 15-20% of redirected orders

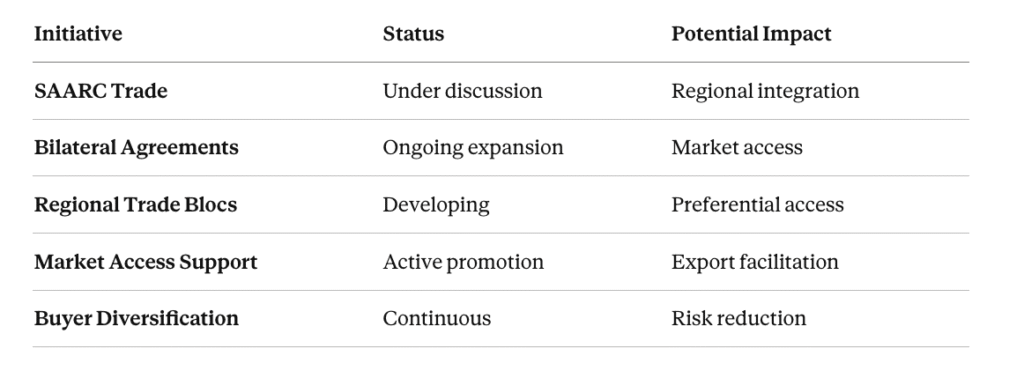

Trade Initiatives & Agreements

10. CHALLENGES, OPPORTUNITIES & FUTURE OUTLOOK

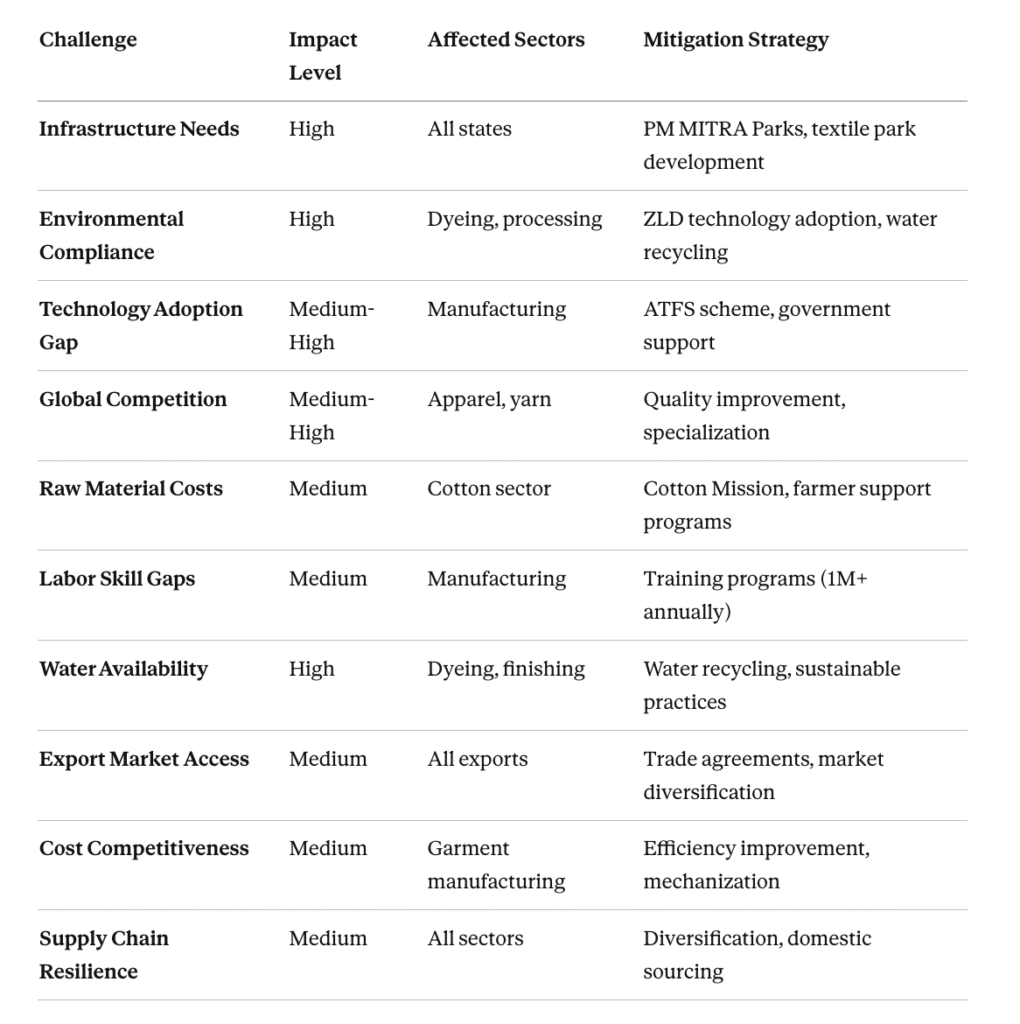

10.1 Current Industry Challenges

10.2 Strategic Opportunities (2025-2030)

Market Expansion

Product & Segment Expansion

Technology & Innovation

- Industry 4.0 integration: AI, IoT, automation

- Blockchain: Supply chain transparency

- Digital supply chains: Real-time management

- Sustainability technologies: ZLD, renewable energy

- Design tools: Digital sampling, 3D modeling

Infrastructure Development

- PM MITRA Parks: Rs 4,445 crore investment

- Textile clusters: State-level development

- Special Economic Zones: Dedicated facilities

- Logistics improvement: Port and rail connectivity

- Digital infrastructure: E-commerce platforms

Domestic Market Growth

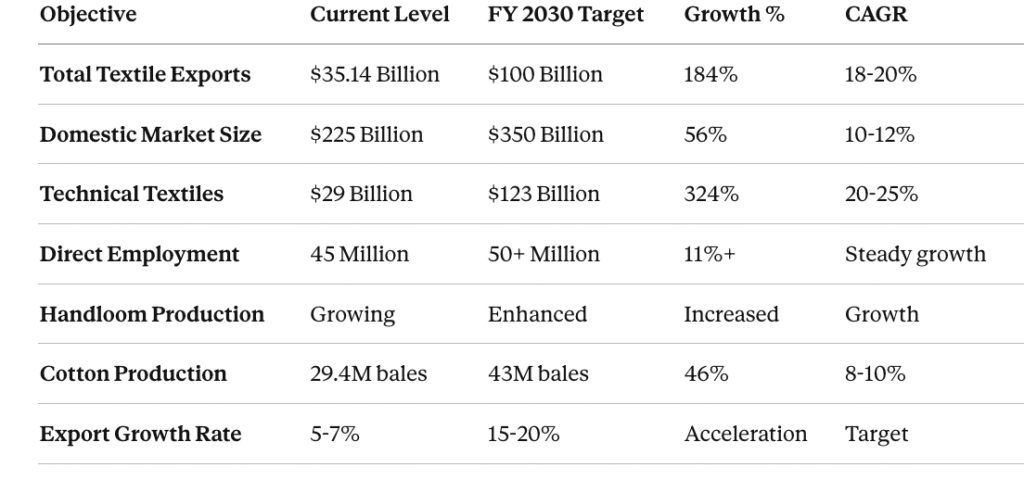

11. VISION 2030 – STRATEGIC OBJECTIVES

11.1 Growth Targets

11.2 Key Growth Enablers

1. Government Support & Policy Framework

2. Infrastructure Development

- Textile Parks: Dahej, Sanand, Surat in Gujarat

- PM MITRA Parks: Multiple locations across states

- SEZs: Special Economic Zones for textiles

- Ports: Improved connectivity for exports

- Logistics: Enhanced supply chain infrastructure

- Digital Platforms: E-commerce and B2B systems

3. Human Capital & Skills

- Workforce: 62% in working age 15-59 years

- Training: 1+ million workers annually

- Artisans: 35.22 lakh handloom workers

- Women Empowerment: 65-72% female participation

- Educational: Textile institutes and colleges

- Vocational: Skill development programs

4. Natural & Raw Material Advantages

- Cotton: World’s largest producer

- Jute: Global leader in jute production

- Silk: Second-largest silk producer

- Wool: Strong wool production base

- Vertical Integration: Fiber to finished product capability

- Cost Advantage: Lower production costs vs developed nations

5. Technology & Innovation

- Industry 4.0: Automation and digitalization

- R&D: Technical textiles development

- Sustainability: Green manufacturing technologies

- Digital Supply Chains: Real-time management

- Quality Systems: International standards compliance

- Design Tools: Modern design and sampling

6. Market Access & Trade

7. Sustainability Focus

- Green Manufacturing: ZLD technology adoption

- Organic Cotton: Certification and promotion

- Circular Economy: Waste reduction and recycling

- Environmental Compliance: National and international

- Social Responsibility: Fair labor practices

- Carbon Footprint: Reduction targets

CONCLUSION

India’s textile industry represents a remarkable fusion of centuries-old heritage and contemporary manufacturing excellence. The sector’s transformation from a traditional craft-based economy to a globally competitive industrial giant demonstrates both strategic vision and operational capability.

Key Takeaways

1. Market Leadership Position: India stands as the world’s second-largest textile exporter with a USD 225 billion domestic market growing at robust 10-12% annually. The industry’s trajectory toward USD 100 billion exports by 2030 and USD 350 billion domestic market by 2030 is supported by strong fundamentals and policy backing.

2. Regional Diversity & Specialization: Tamil Nadu’s dominance in knitwear (26.81% export share with Tiruppur accounting for 90% of cotton knitwear), Gujarat’s manufacturing excellence across cotton, denim, and technical textiles (26.91% export share, 60% denim production), and Maharashtra’s apparel expertise (18.57% export share) create a sophisticated, multi-nodal industrial ecosystem. Contributions from Rajasthan (46% wool), Uttar Pradesh (5th rank), Haryana (4th rank), and emerging hubs like Telangana and Andhra Pradesh ensure comprehensive coverage across product segments and geographies.

3. Employment & Inclusive Development: With direct employment of 45 million people and indirect employment reaching 100 million through allied industries, the textile sector remains India’s second-largest employment generator after agriculture. The significant participation of women (65-72% in various segments), particularly in rural areas, makes textiles crucial for inclusive economic development and women empowerment, addressing structural employment gaps in underdeveloped regions.

4. Technical Textiles Revolutionary Growth: The rapid expansion of technical textiles from USD 29 billion (2024) to projected USD 309 billion (2047) represents a strategic transformation. Growth segments like mobiltech (8.84% CAGR), PPE (10.4% CAGR), and sports textiles (23.9% CAGR) offer exceptional opportunities for value-addition and higher-margin manufacturing.

5. Government Commitment & Support: The 19% increase in textile ministry budget allocation (Rs 5,272 crore), comprehensive schemes (PLI, ATFS, PM MITRA with Rs 4,445 crore), and focused initiatives (District-Led Textiles Transformation, Cotton Mission) demonstrate sustained government commitment. These investments address infrastructure gaps, promote technology upgradation, and support skill development.

6. Global Competitiveness & Market Opportunities: India’s advantages in skilled manpower, cost-effective production, abundant raw materials, and integrated supply chains position it as a preferred manufacturing destination. Recent global dynamics—Bangladesh’s political instability, EU GSP status changes post-2027, rising price parity in key products—create unprecedented opportunities for market share expansion and order diversification.

7. Sustainability & Innovation Focus: Increasing adoption of zero-liquid discharge (ZLD) technology, organic cotton certification, circular economy models, and Industry 4.0 integration demonstrate the industry’s commitment to sustainable, future-ready manufacturing while maintaining cost competitiveness.

Strategic Imperatives for Sustained Growth

- Infrastructure Acceleration: Expedite PM MITRA Park implementation, develop textile clusters, enhance port and logistics connectivity

- Environmental Excellence: Accelerate ZLD technology adoption, water recycling systems, renewable energy integration

- Technology Transformation: Promote Industry 4.0, blockchain implementation, digital supply chain management

- Technical Textiles Development: Increase R&D investment, create specialized manufacturing facilities, develop technical expertise

- Market Expansion: Leverage Bangladesh opportunity, develop SAARC region, expand African and Latin American presence

- Skills Enhancement: Continuous workforce training, focus on emerging technologies, women empowerment programs

- Brand Development: Build Indian textile brands, increase value-added exports, develop design and innovation capabilities

- MSME Support: Strengthen small and medium enterprises, improve access to technology and markets

Final Assessment

The Indian textile industry stands at an inflection point, poised for accelerated growth driven by favorable global dynamics, strong domestic consumption, comprehensive government support, and indigenous innovation capacity. As the industry evolves from volume-based to value-based production, from commodity textiles to specialty and technical textiles, and from traditional manufacturing to Industry 4.0 adoption, it will not only achieve the ambitious Vision 2030 targets but also reinforce India’s position as the “Textiles Land of India” with genuine global leadership in textile manufacturing, innovation, and trade.

The convergence of heritage craftsmanship, modern industrial capability, skilled workforce, policy support, and global market opportunity creates an unprecedented foundation for the Indian textile industry to fulfill its potential as a USD 100 billion export sector by 2030 while maintaining its vital role in employment generation, inclusive development, and rural prosperity.